APRIL 17 2019 – Credit-tech, a highly specialized area of fintech, has significant potential to disrupt the financial industry and will have profound impacts on the credit services providers and credit market especially, according to a new report by Oliver Wyman and China Securities Credit Investment (CSCI).

The report, entitled Technology-driven value generation in credit-tech, reveals that the three layers of China’s credit market – credit assets, credit services, and credit IT – will see significant new business opportunities emerge over the next 5 years benefiting from the credit-tech driven innovations.

Exhibit 1: China’s credit market structure and market size of credit-tech

Layer 1: Credit assets

The report estimates that issuance volume of credit asset in China is expected to grow from 57 trillion yuan in 2018 to 80 trillion yuan in 2022, of which, credit-tech will contribute 54% (43 trillion yuan) in 2022. The strong growth momentum is a result of the gradual expansion of credit services to long-tail customers, including individuals and MSEs that had difficulties in obtaining financing from traditional financial institutions without the solutions provided by credit-tech. As more credit assets are issued, the outstanding balance of credit assets is expected to increase from 144 trillion yuan in 2018 to 195 trillion yuan in 2022, 68 trillion yuan of which will be driven by technology.

The credit trading market is projected to grow from 136 trillion yuan in 2018 to 239 trillion yuan in 2022, 183 trillion yuan of which will be driven by credit-tech. The continuous maturation of both the public and private trading markets will become the major growth driver, and Oliver Wyman expects the contribution of private trading market is more significant. Traditionally, transactions of non-standard assets are difficult to be executed. In the future, however, private trading platforms will be established to increase the transparency of underlying assets, thus boosting the trading volume of non-standard credit assets. The contribution of private market transactions will increase from 16% in 2018 to 24% in 2022.

Layer 2: Credit services

For credit services, the annual revenue will increase from 368 billion yuan in 2018 to 1,034 billion yuan in 2022. Of which, revenue generated by credit-tech will reach 431 billion yuan in 2022, representing 42% of the total amount, indicating a CAGR of 163% from 2018. The credit services market is closely linked to the credit assets market, and most of the service revenue derived from credit-tech services will be related to outstanding balances and new issuances of credit assets.

Layer 3: Credit IT

As the basis and foundation of credit market, credit IT companies help credit-servicing companies improve operational efficiency and service quality by developing credit systems, which is expected to experience an increase in revenue from 9 billion yuan in 2018 to 49 billion yuan in 2022.

“Under the traditional market practices of credit market, companies are required to have solid financial credentials or large scale of assets in order to obtain financing, which has become increasingly inefficient for MSMEs since MSMEs need flexible ways of financing in order to cope with their business needs in China’s changing economic dynamics,” said Cliff Sheng, Oliver Wyman partner and author of the report. “However, startups including CSCI and WeBank are making it easier for companies to obtain financing by leveraging technology to better identify underlying risks, which provides an efficient and scalable solution for MSMEs to thrive.”

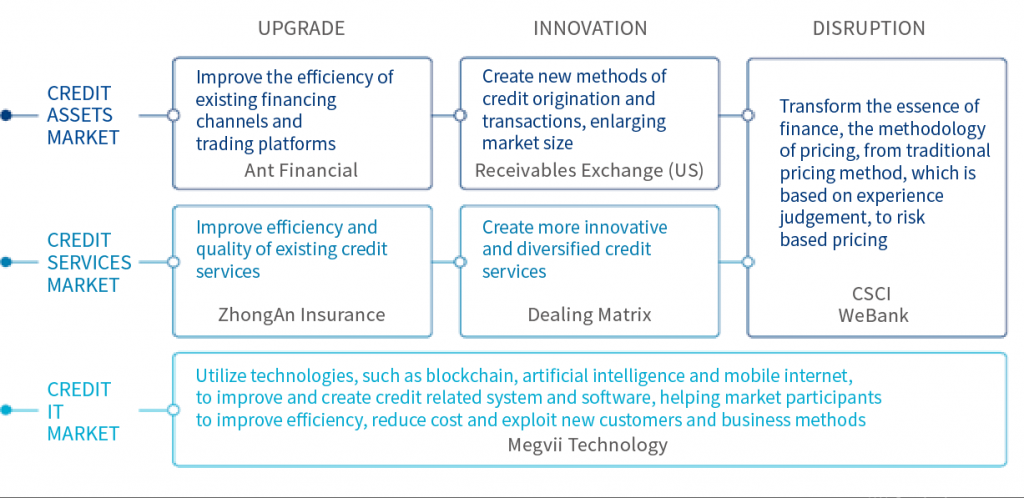

The report also identifies the impacts credit-tech has on the three layers of the credit market in three stages: upgrade, innovation, and disruption (Exhibit 2). Technologies such as the internet, mobile communications, artificial intelligence (AI), blockchain, cloud computing, and big data analytics will reshape and disrupt the financial industry, and will have profound impacts on credit service providers and credit market especially.

Exhibit 2: Impact of credit-tech on credit-related markets

According to Cliff Sheng, in China, key drivers of the credit-tech market are macro-economic factors including the fast-growing financing volume and structural reform of the macro-economy, improving market maturity and efficiency as a result of regulation, and the development of new technologies such as AI, blockchain, cloud and big data. While the main players in the market are traditional financial institutions, fintech players, and technology companies, the report also underlines that only those companies with the following characteristics can be successful:

• Strong integration across technology, business know-how, branding, and resources

• A market-oriented operating model

• An internet start-up culture

• Competitive talent propositions and incentive schemes.

Together these will set apart the eventual winners excel its peers and capitalise on the opportunities arising from the new technologies and become pioneers of sector over the next 5 years.

About the report

The report titled Technology-driven value generation in credit-tech provides an overview of the credit-tech market in China and discusses how credit-tech will reshape and disrupt the financial industry, especially for the credit services providers and credit market. The first section defines credit-tech and shows its main impacts on the three layers of the credit market: credit assets, credit services, and credit IT. The second section provides an in-depth analysis of the credit-tech market in China and quantifies the potential impact of credit-tech. Firstly, the addressable market size of the three layers of credit market were identified. Then, the respective market size driven by credit-tech was calculated. The report also highlights the key success factors for leading credit-tech players.

Link to download the full report:

https://www.oliverwyman.com/our-expertise/insights/2019/apr/china-credit-tech-market-report.html

About Oliver Wyman

Oliver Wyman is a global leader in management consulting. With offices in 60 cities across 29 countries, Oliver Wyman combines deep industry knowledge with specialized expertise in strategy, operations, risk management, and organization transformation. The firm has more than 5,000 professionals around the world who work with clients to optimize their business, improve their operations and risk profile, and accelerate their organizational performance to seize the most attractive opportunities. Oliver Wyman is a wholly owned subsidiary of Marsh & McLennan Companies [NYSE: MMC]. For more information, visit http://www.oliverwyman.com. Follow Oliver Wyman on Twitter @OliverWyman.

About CSCI

CSCI is a leading integrated credit-tech services provider. Empowered by its technology, CSCI establishes credit infrastructure services throughout the credit asset life cycle. CSCI offers tailored solutions for its clients, which helps reduce the cost of credit risk management, lower credit asset investment risk and increase credit asset turnover rate. For more information, visit https://www.chinacsci.com/en/